The tenth of ten deep-dives in our 2026 delivery trends mid-year check-in: AI discovery surged, ChatGPT scaled back direct checkout, and merchants kept the delivery promise.

Our 2026 trends report predicted that AI-mediated shopping would change how people discover, buy, and receive orders, and that retailers would need their product, price, delivery, and returns data structured well enough for machines to read.

What we said in early 2026

AI-mediated shopping, omnichannel behavior, and cross-border demand would reshape how people discover, buy, pay, and receive orders, and retailers would need product, price, delivery, and returns data structured enough for machines to read. Our New Retail Reality report went further: the battleground shifts to operational legibility, where brands whose delivery terms cannot be evaluated by an agent become easier to exclude without a human ever seeing the brand page.

Six months on, this trend moved fastest out of our 10-predictions set, and in the most decisive way:

-

AI-led discovery grew quickly, but delegated checkout, the part where an agent completes the purchase for you, did not take hold the way many expected: ChatGPT scaled its direct checkout back toward conventional merchant journeys, while other agentic-commerce protocols kept developing.

-

Merchants, for now, still hold the transaction, and with it the delivery promise. And the consequence for anyone who ships is: the delivery data you expose to a machine has become demand infrastructure, and retailers should check what a machine can read from their offer today.

What AI shopping actually became in 2026

AI shopping is the shift of product discovery and comparison out of the search box and the category page and into AI assistants: a shopper asks an assistant for a recommendation, and the assistant reads across retailers to answer. In 2026, the striking part is what did not happen.

Assistants became a fast-growing discovery channel, but agent-completed checkout did not become the norm. The most visible experiment, agents completing purchases end to end, pulled back toward merchant checkout, while other protocols kept being tested.

The common pattern today is the agent recommending and comparing, then handing the shopper to the merchant's own checkout to buy, though the market structure is still unsettled rather than fixed. For a delivery business, that pattern decides who is reading your delivery terms, and when.

AI discovery became a measured channel, fast

The scale is no longer speculative, though it needs reading carefully. Salesforce put AI and agents behind 20% of retail sales during the 2025 holiday season, around $262 billion. That figure is broad: it spans AI across commerce, including retailers' own recommendation engines and on-site agents, not third-party assistants alone.

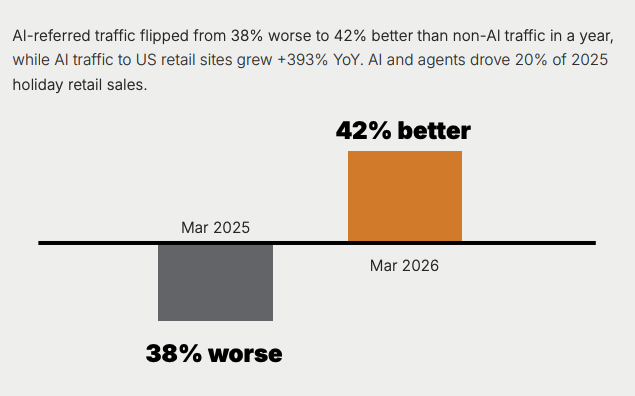

The evidence specific to outside AI discovery comes from Adobe, which measured traffic from AI sources to US retail sites growing 393% year over year in the first quarter of 2026, and found that by March it converted 42% better than non-AI traffic, a reversal from a year earlier when the same traffic had converted 38% worse.

Salesforce adds one more marker on that channel: shoppers arriving from AI-powered search converted roughly nine times more often than those referred from social media. In two quarters, third-party AI discovery went from a curiosity to a measured acquisition channel.

DHL's 2026 e-commerce research frames the same shift from the carrier side, arguing that the old rules do not apply once AI moves into the buying decision itself.

20%

of 2025 holiday retail sales were influenced by AI and agents

Around $262 billion, per Salesforce.

+393%

growth in AI-referred traffic to US retail sites, year over year

First quarter of 2026, per Adobe.

42% better

how AI traffic converted by March 2026

A year earlier the same traffic converted 38% worse.

The inversion: discovery moved, the promise stayed

The clearest signal came in March, when OpenAI deprecated its Instant Checkout program after fewer than 30 Shopify merchants had ever gone live, and pivoted ChatGPT shopping to discovery plus a redirect into the merchant's own checkout. That is one company's move; other agentic-commerce and payment protocols are still live and being tested, as we cover in what agentic commerce is. But it is a telling move: OpenAI's version of the near future is an agent that owns discovery and hands the customer back to the merchant to convert.

It would be easy to read OpenAI's pivot as the pressure coming off, since merchants keep running their own checkout. It does the opposite: wherever an agent recommends and the merchant converts, the delivery options, dates, fees, and returns terms the agent could read are part of what decides whether the customer is ever sent your way. A vague or unreadable delivery proposition can cost you the recommendation itself, before any conversion math runs, and before a human ever sees your brand page.

The battleground moves to operational legibility, where a brand whose delivery terms an agent cannot evaluate becomes easy to exclude without anyone deciding to exclude it.

The agent-legibility test most retailers have never run

Legibility here has a specific meaning: whether a machine can read your delivery options, dates, fees, and returns terms, in a structured form, and evaluate them against a competitor's. Not whether a person can see them on the page, but whether an agent can parse them without guessing.

Adobe puts the average retail product page at about 66% on its measure of AI visibility, a machine-readability score for how much of a page an automated system can reliably interpret, rather than a literal count of hidden content. A large share of retail pages are only partly legible to the systems now doing the first pass of shopping.

Delivery terms are among the least structured parts of most checkouts, because they are often assembled at runtime from carrier rules, cut-off logic, and postcode lookups, and rendered for human eyes rather than exposed as data.

Running the test properly means separating two layers, because a general-purpose assistant cannot be assumed to crawl or execute a dynamic checkout widget.

-

The discovery layer: what an assistant can read about you before any checkout, such as your standard delivery options, the markets you serve, your delivery and returns policies, and the logic behind your pricing, in a form that does not depend on a session or a filled basket.

-

The quote layer: whether a supported partner, protocol, or API can request a specific delivery promise for a real basket to a real postcode, and get back the service, price, ETA, conditions, and returns method as structured data. A usable quote interface has a stable shape on both sides. The inputs it accepts are defined: the destination market, the postcode, the basket contents, and any service constraints. The outputs it returns are defined too: a stable option identifier, the price, the ETA, the conditions attached, and the returns method.

Most retailers have some of the first layer as page text and almost none of the second as an interface. Where the promise is only computed after a shopper has entered enough detail to reach the delivery step, an agent comparing you against alternatives has nothing clean to read at either layer, and falls back on whatever it can parse elsewhere. A promise passes the test when it is expressed clearly enough for a machine to read, and kept reliably enough afterward to be worth reading.

Structured, here, does not mean elaborate. It means the delivery promise exists as data an agent can request and compare: an option with a name, a price, a delivery date or window, any conditions attached, and matching returns terms, rather than a block of text rendered for a browser or a widget that only resolves once a person clicks through. This is the same data a good human checkout already relies on to show accurate dates and costs. The work is exposing it, not producing something new. A retailer whose checkout already computes an honest, specific promise for a person is most of the way to one a machine can read.

The economics: legible promises win twice

The networks that can expose an accurate, machine-readable promise, and then keep it, win in two places at once:

-

with the agent that decides whether to surface them

-

with the human the agent is shopping for

The same structured delivery data that makes you legible to an assistant is the data that lets you show an accurate date and hold it, so the customer returns for a second purchase.

Illegibility costs in a way the old funnel did not: a weak delivery promise used to cost you at the cart, where at least the abandonment was visible and you could try to fix it. In an agent-mediated funnel it costs you earlier and less visibly, in recommendations that never happen, with exclusions applied upstream of anything your analytics can see.

That's a probably tougher problem than cart abandonment - there is no event to diagnose, only demand that fails to arrive with no trace to follow. The advantage, for now, is that most retailers have never run the legibility test, so the one who makes its promise readable early is competing against a field that has not started.

Illegibility costs in a way the old funnel did not.

There's also a budgeting implication most teams have not caught up to. If AI-referred traffic converts far better than social and better than a site's own baseline, that channel deserves deliberate investment rather than incidental effort. In practice, that means giving agent-readiness a named owner, tracking it with its own channel metrics, and running the legibility audit on a defined schedule, set alongside the rest of the acquisition budget rather than left to whoever last touched the checkout. I believe very few retailers have put that in place yet.

Returns complete the offer an agent needs to compare

The delivery promise an agent evaluates does not stop at the outbound date. Returns terms, whether returns are free, how they are made, and how long a refund takes - all these are part of what makes an offer safe to accept. There's more evidence here tied to people rather than agents so far: the IPC finds that clear delivery-charge information before purchase is essential to a majority of cross-border shoppers, and DHL's 2026 research points to easy returns as a conversion factor.

Even if assistants don't weigh returns terms directly yet, if an assistant cannot compare your full offer against a competitor's without the returns terms, the consequence is the same - leaving them out of the machine-readable promise means being compared on an incomplete version of what you offer. Exposing returns terms alongside delivery terms, as structured data rather than a policy-page link, is what lets the comparison be made on your real proposition.

Cross-border demand moved at the same time

The interface was not the only thing shifting; demand moved geographically, too. As US tariffs bit, Temu's EU sales growth surged past 60% year over year by early May, approaching 100% in France, while Shein's UK growth ran around 50%.

The IPC's cross-border shopper survey, which covered nearly 31,000 consumers across 37 countries, found Temu alone now accounts for roughly a quarter of the most recent cross-border purchases, and that 61% of shoppers rate clear information on delivery charges before purchase as essential.

The same survey shows expectations tightening on speed as well as clarity: the share of cross-border parcels taking 15 or more days fell from 29% in 2020 to 7% in 2025. That shift raises a practical planning question for European retailers and carriers: whether their customs, capacity, and delivery-cost logic can absorb more price-sensitive cross-border demand, at the same time as the EU's temporary €3 customs duty on goods under €150 from non-EU IOSS sellers goes live from 1 July.

For European retailers, cross-border price competition intensifies while landed cost, the total a customer pays including duty and delivery, now has to be transparent at checkout rather than a surprise at the door. That the surprise drives returns and lost trust is well supported by the shopper data; an inaccurate landed cost is a risk with agents as well as people.

We go deeper on the cross-border operating shift in our piece on cross-border ecommerce logistics in 2026 and on the post-checkout experience that keeps those customers.

Record volume is not the same as promises kept

Through all of this, carriers processed record volumes around Black Friday 2025:

-

DHL handled more than 14 million shipments on its busiest day, around 60% above an average day

-

Deutsche Post's parcel network processed roughly 12.4 million shipments in a single day

European B2C e-commerce had already grown 7% in 2024 to €842 billion, and the 2025 peak confirmed that the demand base keeps compounding through every shock.

But a record day measures throughput, not promise accuracy. It says nothing about how many individual delivery promises changed underneath it, how many exceptions were caught in time, or how many returns resolved cleanly. Those are measured order by order, and in an agent-mediated market the cost of a missed promise lands on the brand that made it, not in the carrier's volume statistics. The demand is compounding; whether each promise is kept is a separate question, and it is the one that carries into the next recommendation and the next purchase.

The promise now has to travel across surfaces

Discovery is fragmenting across more surfaces than AI assistants alone. IAB Europe's January 2026 industry survey ranks retail and commerce media just behind connected TV and AI among the year's top growth opportunities, with off-site and omnichannel placements named as the expansion frontier.

A product now gets discovered in an assistant, a retail-media placement, a marketplace, and a social feed, and the delivery promise attached to it has to read the same, and be as trustworthy, in every one of them. A promise that is clear on your own site but garbled everywhere else a machine encounters it is only doing part of its job. The requirement under all of these surfaces is the same structured, accurate delivery data.

Legibility is one face of the orchestration gap

A promise that is legible to a machine and kept for a customer is the visible output of everything behind it working together: checkout showing what the network can execute, carriers reporting events cleanly enough to keep the promise current, returns feeding back into the same record. Our own research calls the space where those connect the orchestration gap, and this trend is where it surfaces as revenue. A retailer can expose a clean, structured promise and still lose the customer if the operation behind it cannot keep it. Legibility earns the recommendation; execution keeps it.

What to do before peak

First, run the agent-legibility audit across both layers.

-

On the discovery layer, confirm that your standard options, served markets, delivery and returns policies, and pricing logic are readable without a session, not buried in a widget.

-

On the quote layer, confirm that a supported partner, protocol, or API can request a basket- and postcode-specific promise and receive the service, price, ETA, conditions, and returns method as structured data.

Keep cross-border landed cost transparent at checkout, ahead of and through the July duty change, so the total a customer commits to is the total that arrives. A surprise at the door is now a returns event and a lost recommendation, not only a complaint.

Remove the manual work that caps how many markets you can serve. Maya Delorez, a Swedish equestrian brand running on our platform, ships to roughly 80 markets a month without manual shipping administration, which is the operating shape cross-border demand now rewards.

Customers experience all of logistics as one promise.

nShift's Checkout and Track work at the two ends of that promise.

nShift Checkout helps retailers configure and display delivery options, prices, ETAs, and the rules behind them at the point of sale.

nShift Track provides normalized delivery events and proactive customer updates after it.

Neither makes a retailer agent-legible on its own; that still takes exposing the promise as data through the layers above. They provide the delivery options, rules, and post-purchase events that a retailer can expose through the appropriate data and integration layer.

The agentic readiness of that promise is the same question we examine in the agentic readiness gap.

The single promise

Customers experience all of logistics as one promise: the date they were shown, and whether it held. What changed in 2026 is that a machine now reads that promise first, and decides whether the customer ever sees it. The retailers pulling ahead are not the ones with the most delivery options or the fastest service. They are the ones whose promise is structured enough for an agent to read and reliable enough to keep. The first comparison may be machine-assisted. The delivery experience is still judged by the customer, in the date, update, and return that follow.

For the full mid-year check-in across all ten trends, read the full midyear trends report.

More from the mid-year check-in:

- Logistics APIs in 2026: why integration decides how fast you can launch

- Ecommerce delivery options in 2026: choice, conversion, and returns

- Supply chain resilience in 2026: when trade policy became the disruption

Ten trends. One mid-year evidence check.

Get the full 2026 delivery logistics mid-year check-in, with the data and recommendations behind all ten trends.

Get the report